Is Inflation Transitory and Can the S&P 500 Hold the Line? By Van Tharp Trading Institute

Many folks in the U.S. are returning to summer travel schedules. And like so, so many other things – the cost of travel has skyrocketed.

In late May of 2019 (before COVID), my wife and I spent a week on the Gulf Coast of Florida for a little R&R. We rented a car at the Tampa airport, for a week, at a total cost of $150.82 (no additional insurances purchased).

Earlier this week, I made the exact same reservation. I rented the same car class, at the same airport, on the exact same week. And the all-in cost? $447.66 – a stunning triple increase in price vs. the same week pre-COVID.

There are many reasons for a higher cost on the rental – the bankruptcy liquidation from top dog Hertz, COVID fleet reduction across the rest of the players, and reduced car availability thanks to the automotive semiconductor shortage.

But three times the price is a huge jump. To be fair, the rental properties I saw are only up 25-50%, and our airfare is practically identical from two years ago. But there is no doubt that inflation has reared its ugly head. Lumber futures prices are up 280% since this time last year. That means no new deck in 2021 for the Barton family…

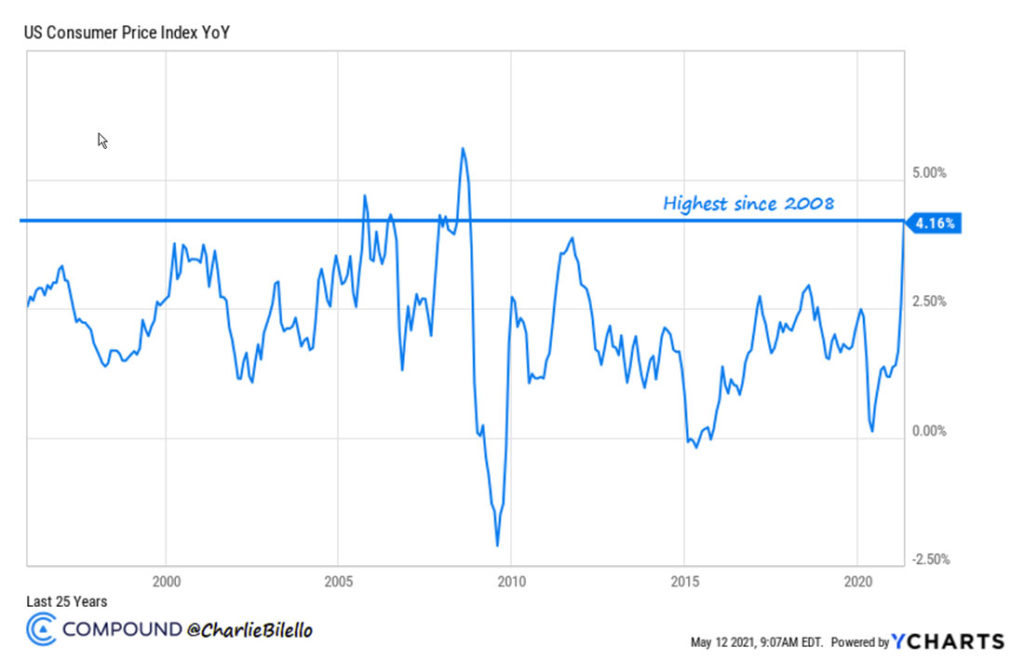

And finally, the Consumer Price Index (CPI) jumped 4.2% this morning (May 12) – a climb we haven’t seen in over a decade as shown by this chart from Charlie Bilello at Compound Advisors:

The Fed has already said they will not act to slow inflation in the near term, calling it “transitory” due to supply and demand imbalances caused by COVID.

I have heard it said that a reversal from decades-long low (sub 2%) inflation would be a generational event impacting financial markets and portfolio make-ups. I very much believe this is true. In the coming months, I’ll be writing a lot about additional inflationary signposts to watch and more importantly, what changes (if any) need to be made long-term in investments like retirement nest eggs.

For today, I believe the big question is whether this inflation is really transitory in nature as the Fed espouses and whether this resilient bull market will quickly forget these numbers and resume its climb. Due to the influence of very accommodative monetary policy and the spending proclivity of the current White House and Congress combo, I believe that the probabilities lie in this pullback being another shallow one, and therefore quick-tradeable.

Here’s the near-term support level in the S&P 500 that should hold if the bull is to resume:

Van Tharp Trading Institute June 09 Peak Performance 101 Streaming Workshop